Warranty & Service16 min read

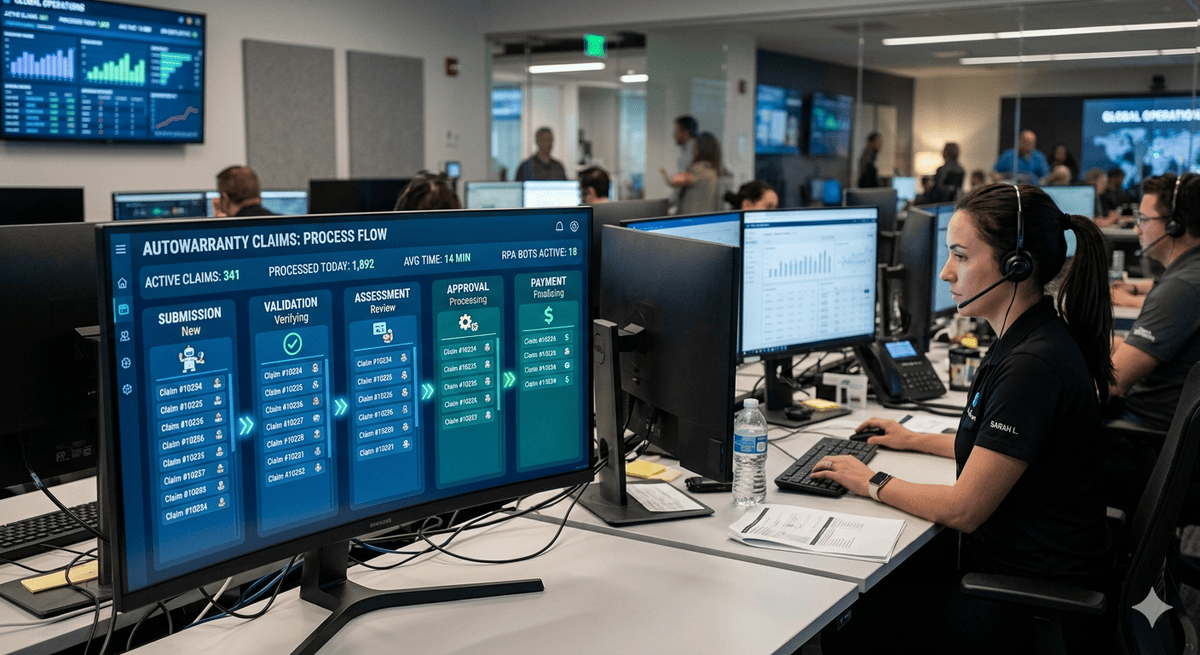

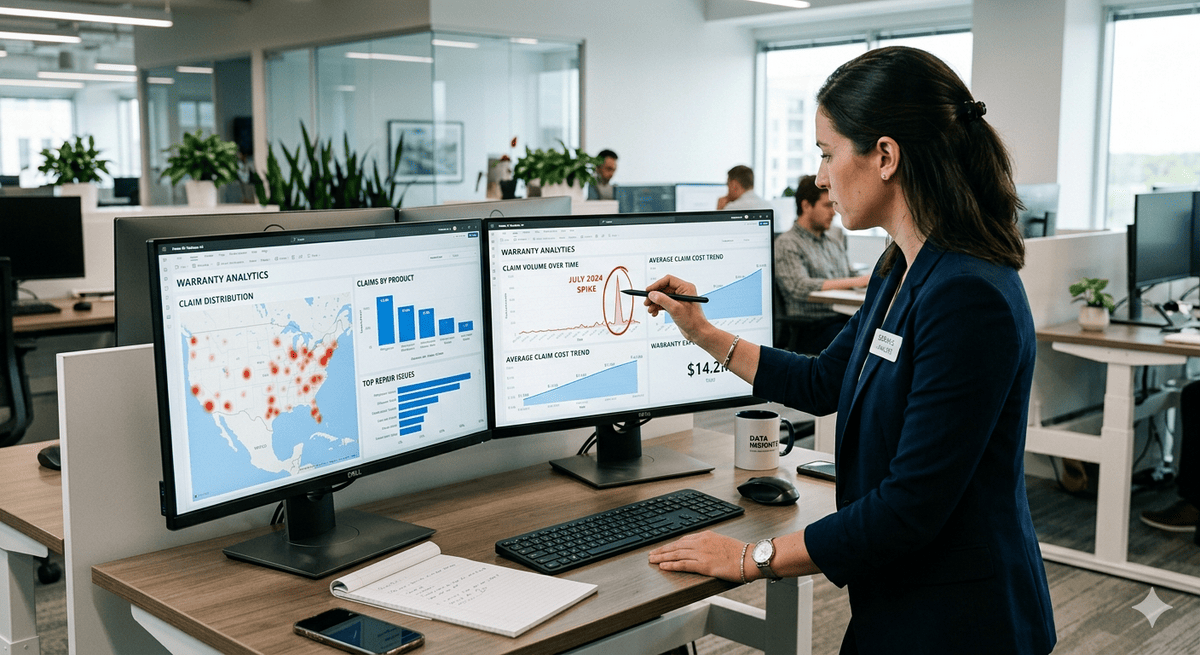

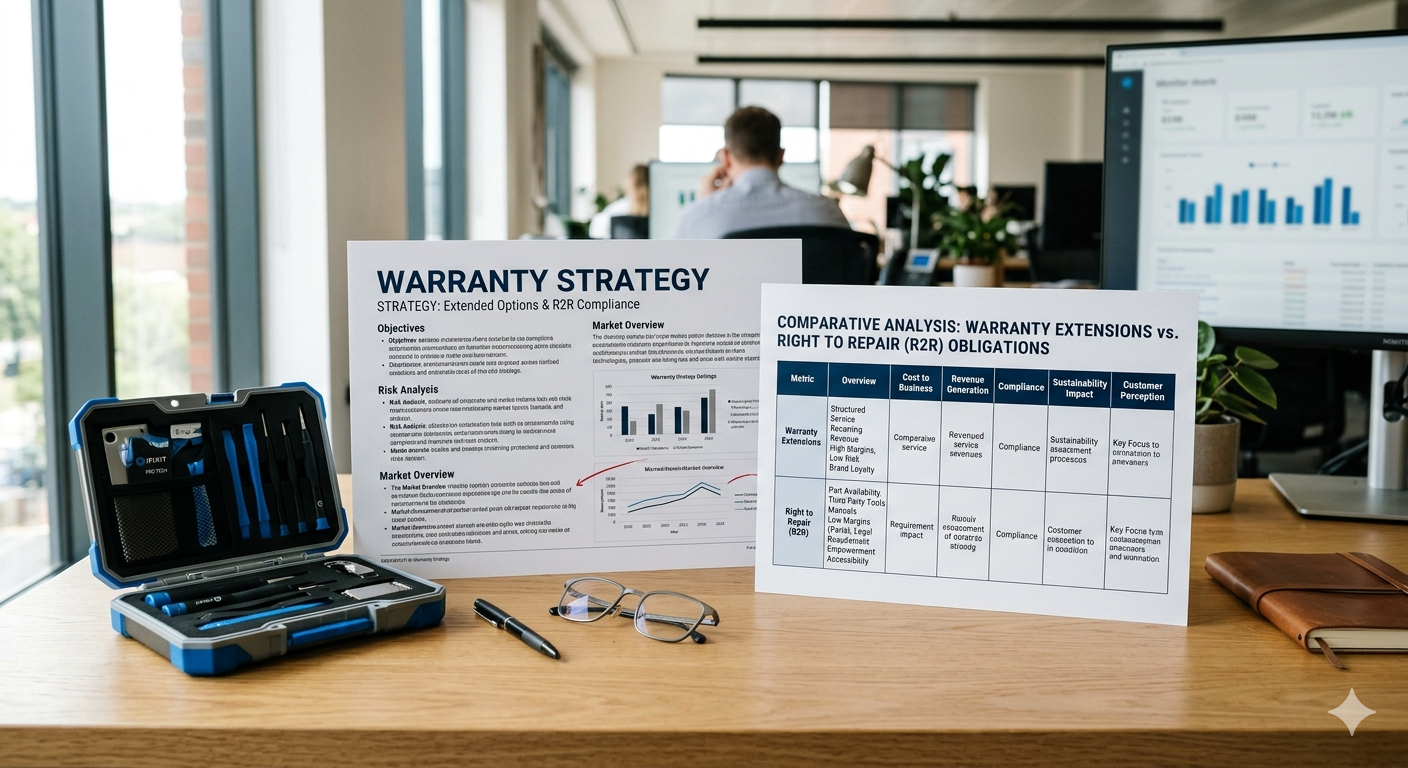

Warranty Analytics: What Your Data Should Actually Tell You

Most warranty dashboards show raw counts. Here's what world-class warranty analytics looks like — and why your current tool is hiding the most valuable signals.